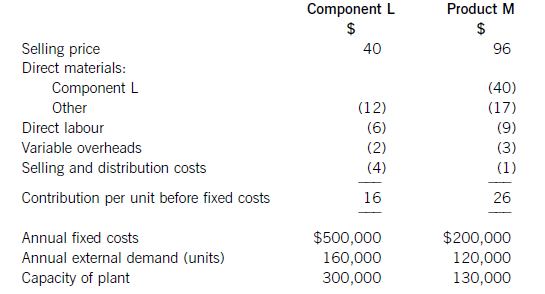

题目内容

(请给出正确答案)

题目内容

(请给出正确答案)

Branscombe Co has been supplying and fitting premium bathrooms and kitchens in hotel chain

To remain fully compliant with the Effland corporate governance code, the board established audit, remuneration and nomination committees which were solely populated by independent non-executive directors. However, it did not consider it necessary to create a separate risk committee because the board believed that the remit of the audit committee included all aspects of risk management policy. This explanation was formally submitted to the shareholders at its first general meeting, who agreed with the board’s proposal.

As part of its expansion strategy, the board of Branscombe Co decided it needed to enter overseas markets, and in particular the developing country of Geeland. The reason that Geeland was selected as a suitable market was because it had experienced rapid economic growth and domestic prosperity following the discovery of rich, offshore mineral deposits. Unfortunately, this small island nation has never enjoyed stable democratic government and is notorious for corrupt business practices, with customs officials regularly demanding bribes from both importers and exporters. As a result, Geeland has a poor international credit rating. In order to attract both domestic and foreign inward investment, the government of Geeland operates with very low levels of indirect tax, which has stimulated the island’s tourist industry and led in turn to a significant increase in hotel building.

Following a successful tendering exercise, Branscombe Co was awarded the contract to supply all of the bathroom equipment for a 200-room hotel, currently under construction in a remote area of the island. The total value of the supply contract amounted to Geeland $1,800,000, and it was to be paid in three equal instalments as the bathrooms were delivered to the hotel. The contract assigns responsibility for shipping the goods the 3,000 km from Effland to the island solely with Branscombe Co, and no payment will be made until an agreed volume of goods clears Geeland customs. A further problem is that the Geeland dollar is quite volatile, but recently it has been strengthening against the Effland dollar. As all contract payments are to be made in Geeland currency, Branscombe Co is exposed to foreign exchange risks.

The many contract-related issues amount to significant risks to Branscombe Co requiring effective management if the supply contract is to be a success and contribute to the company’s ambitious growth targets.

Required:

(a) Explain the function and roles of a risk committee within an effective corporate governance framework, and discuss the advantages which a risk committee could add to the governance of Branscombe Co. (10 marks)

(b) Explain the term risk appetite, and assess how the risk appetite of Branscombe Co has influenced both its corporate strategy and the risks it has chosen to bear. (7 marks)

(c) Explain how Branscombe Co could effectively control the strategic and operational risks which arise from the Geeland supply contract. (8 marks)

如果结果不匹配,请 联系老师 获取答案

如果结果不匹配,请 联系老师 获取答案

更多“Branscombe Co has been supplyi…”相关的问题

更多“Branscombe Co has been supplyi…”相关的问题